AI in Insurance Claims 2026: Tractable, Snapsheet, and the Straight-Through Reality

Production AI in insurance claims in 2026 — Tractable, Allstate Drive AI, USAA, Snapsheet, Hi Marley, ClaimVantage, Shift Technology — and the gap between straight-through processing demos and lived loss-ratio outcomes.

Insurance claims is where insurers most want AI to work and where they have spent most aggressively. The reason is simple — loss adjustment expense (LAE) is the largest controllable cost in claims handling, and even a few percentage points of operational efficiency compound enormously on a large book.

By 2026 the AI claims story has matured from the breathless 2022 pitch decks into a more honest picture. Some workflows are genuinely straight-through. Others are AI-assisted with humans in the loop. A few have gone backwards because the early automation hit edge cases that were expensive in customer experience and regulatory attention.

The vendor landscape#

Tractable remains the most visible name in claims AI, with computer vision over vehicle damage photos powering first notice of loss triage and estimate generation. Tractable’s product is embedded in workflows at Tokio Marine, Geico, Allianz, Mitchell, and several others. The honest accuracy in 2026 is good enough for total loss decisioning and for damage triage; estimate-level accuracy that matches a human appraiser is closer than it was but still not the default for high-severity claims.

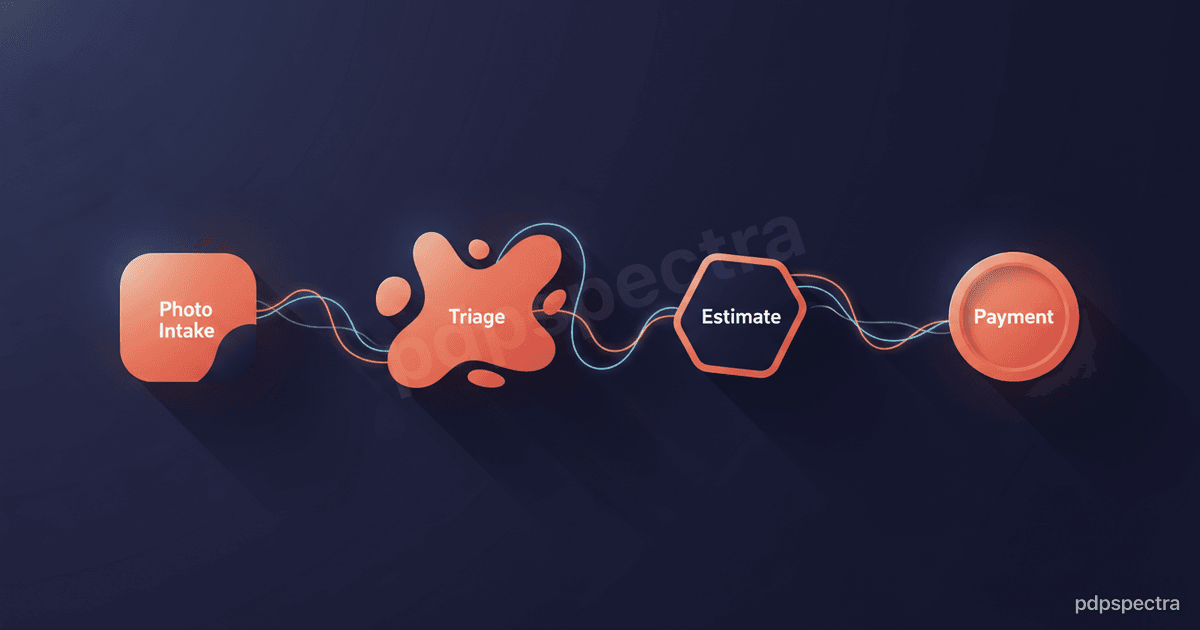

Snapsheet built the original virtual appraisal workflow and operates as a BPO plus software stack — claimants submit photos via an app, Snapsheet’s combination of AI and remote adjusters produces estimates, the carrier accepts or rejects. Snapsheet is used by many regional carriers and several large ones for specific lines.

CCC Intelligent Solutions is the incumbent in auto estimating with Mitchell as the other major incumbent; both have aggressively layered AI into their estimating platforms, and the practical reality is that most US auto claims touch one of these platforms at some point.

Hi Marley built the messaging platform for claims communication — SMS and chat between adjuster and policyholder — and has been adding AI summarization, drafting, and routing on top. The reason this matters more than it sounds is that adjuster time on phone and email is one of the largest cost drivers in claims, and the messaging surface is where AI assistance shows up most usefully.

ClaimVantage (acquired by Majesco) is the established life and disability claims platform; AI shows up in document classification, evidence sufficiency, and decision support.

Shift Technology is the most prominent fraud detection vendor, with hundreds of insurer deployments globally for SIU triage, network analysis, and suspicious claim flagging. Friss (Netherlands-based) is the European counterpart with strong traction.

What “straight-through processing” actually means in 2026#

The phrase straight-through processing (STP) is used loosely. The clean version: a claim is reported, triaged, valued, decisioned, and paid without a human touching it. The reality of 2026 STP rates:

For glass-only auto claims, STP rates above 70 percent are common at carriers with mature integrations. For small-value renters and homeowners claims (single appliance, basic theft), STP rates above 50 percent are achievable. For full auto physical damage, STP rates of 15 to 25 percent are realistic. For high-severity, bodily injury, or third-party liability claims, STP is essentially zero and will remain so for the foreseeable future.

The carriers that publish STP numbers tend to be selective about which segments they report on. The full-book STP rate at a large mixed-line carrier is meaningfully lower than the cherry-picked segment numbers in vendor marketing.

Allstate’s Drive AI and the OEM-data angle#

Allstate’s Drive AI (formerly Arity-powered, now broader) is one of the more interesting carrier-side programs because it spans pricing, claims triage, and crash detection. The crash detection piece is the meaningful one — telematics-detected crashes that trigger immediate outreach and pre-fill claim data before the customer even opens the app. Several other carriers (State Farm, Progressive) have analogous capabilities.

The broader OEM-data trend is that Tesla, GM, Ford, Stellantis, and the Korean and Japanese OEMs all have varying degrees of post-collision data they can share with carriers under the policyholder’s consent. The integration work is non-trivial and the consent flows are scrutinized by privacy regulators, but the data quality is meaningful and the trend is real.

USAA and the closed-ecosystem advantage#

USAA is consistently cited as one of the most successful carrier-side claims AI programs, and the reason is structural — USAA’s membership is closed and tightly identified, the relationship is multi-line (auto, home, life, banking), the lifetime value justifies serious investment, and the customer trust is unusually high so customers willingly share photos, location, and post-incident data.

The practical effect is that USAA can run claims triage and decision flows that look enviable from the outside but are very hard to replicate at a carrier with a more transactional customer relationship.

Fraud detection and the SIU workflow#

Shift Technology and Friss dominate the dedicated fraud vendor segment but most of the actual fraud detection work in 2026 is done by carrier-internal models tuned to their book and integrated with the SIU (special investigations unit) workflow. The mature pattern looks like:

A risk score is computed at FNOL and updated as evidence accumulates. High-risk claims are routed to SIU; medium-risk claims are flagged for adjuster attention; low-risk claims proceed normally. The AI augments rather than replaces SIU investigators. Network analysis (the same claimant, repair shop, and medical provider appearing across multiple claims) is one of the most productive techniques and has been since well before deep learning. LLM-augmented narrative review is the newest layer and is being adopted carefully.

The biggest fraud detection failure mode is excessive false positives that delay legitimate claims and trigger regulatory complaints. The carriers that get this right tune aggressively for precision rather than recall in the customer-facing decision path.

The hard segments#

Commercial property claims (catastrophe events, business interruption) remain heavily human. The dollar amounts are large, the legal exposure is meaningful, and the variance across claims is high. AI shows up in triage and document handling but the decisioning is human.

Casualty and bodily injury claims are similarly human, and the time-to-settlement is measured in months or years rather than days.

Workers’ compensation is partially automated for indemnity-only claims and barely automated for the more complex medical-management cases.

What changed in 2025 and 2026#

Two shifts worth noting. First, generative AI moved from claim adjuster co-pilot demos into actual deployment for narrative drafting (denial letters, status updates, internal notes). The deployment is carefully governed because the legal exposure on a poorly worded denial is meaningful.

Second, the EU AI Act and state-level US regulation pushed carriers to formalize human-in-the-loop documentation. The lesson several carriers learned the hard way is that “the model recommended denial” is not a defensible audit trail; “the model surfaced these specific risk indicators, the adjuster reviewed them, the adjuster signed the decision” is.

Where pdpspectra fits#

Our AI integration practice helps insurance carriers and InsurTech platforms build production claims systems — vision integration, document AI, fraud scoring, and the audit and governance scaffolding that production claims AI requires.

Related reading: insurance claims vision AI for the adjuster, the AI insurance claims and underwriting post, and climate risk analytics for finance and insurance.

Claims AI is real, partial, and bounded by edge cases that are expensive in customer experience. Talk to our team about your claims AI roadmap.