Satellite Constellations in 2026: Starlink, Kuiper, OneWeb, IRIS², AST

Starlink, Kuiper, OneWeb / Eutelsat, Telesat Lightspeed, SES O3b mPower, IRIS² European sovereign constellation, AST SpaceMobile — the 2026 constellation map.

The satellite constellation map in 2026 is more crowded than it has been in any prior year and still not as crowded as the filings suggest it will be by 2030. Starlink dominates by operational scale. Project Kuiper is in early build-out. OneWeb absorbed into Eutelsat, Telesat Lightspeed shifted focus, SES merged with Intelsat, and the European IRIS² sovereign constellation is in active development. AST SpaceMobile and Starlink Direct-to-Cell define the cellular-from-space category. Underneath everything, GEO operators are pivoting from broadband to mobility and broadcast.

This is the 2026 map — who’s flying what, what they’re flying it for, and how the economics differ.

The LEO broadband competitive picture#

The headline LEO broadband market in 2026:

- Starlink — roughly 7,000 active satellites, 6M+ subscribers, global coverage, the operational benchmark

- Project Kuiper — Amazon’s constellation, hundreds of satellites in early 2026, scaling toward 3,236 by 2029

- OneWeb (Eutelsat OneWeb) — ~650 active satellites, enterprise-focused, completed first-generation deployment, merged into Eutelsat in 2023

- Telesat Lightspeed — Canadian, smaller constellation of ~200 satellites planned, enterprise and government focus, deployment timeline slipped

- Guowang and Qianfan (China) — Chinese national constellations, deployment accelerating but limited transparency on operational scale

The competitive shape is two-tier. Starlink and Kuiper are the consumer-and-enterprise scale plays. OneWeb, Telesat, and the Chinese constellations are differentiated by enterprise, geography, or sovereign focus.

Starlink’s operational lead#

Starlink’s lead in 2026 isn’t just satellite count — it’s terminal availability, software maturity, billing and operations infrastructure, and the iteration speed of the constellation. SpaceX launches Starlink missions at roughly weekly cadence. V2 Mini satellites have laser inter-satellite links that route traffic between satellites without ground-station hops, enabling polar coverage and reducing terrestrial-network dependency.

The deeper economic advantage: Starlink benefits from Falcon 9 reuse and Starship coming online. Per-launched-satellite cost continues to fall, and that compounds in subscriber economics. Competing constellations either build cheaper satellites (hard) or pay SpaceX to launch them (Kuiper has bought Falcon 9 launches).

Project Kuiper: Amazon’s catch-up#

Kuiper started flying real satellites in 2024 and accelerated through 2025-2026. Amazon has FCC obligations to launch half the constellation by July 2026 and the full 3,236 by 2029. The pace question is real — Amazon is behind, and the launch capacity to catch up is constrained.

The differentiated story for Kuiper:

- AWS integration — Kuiper traffic enters AWS via direct fibre interconnect with deep cloud integration

- Enterprise channel — Amazon’s existing enterprise and government sales motion

- Multi-launch strategy — Atlas V, Vulcan, Ariane 6, plus SpaceX, hedging against any single launcher

The 2026 question is whether Kuiper closes the gap fast enough to be a competitive alternative to Starlink for enterprises that want a second source. The 2027-2028 picture will tell.

OneWeb / Eutelsat: enterprise-only by design#

OneWeb completed its first-generation 650-satellite constellation in 2023 and merged with Eutelsat in 2023 to form Eutelsat OneWeb. The strategic posture: enterprise-only, no consumer broadband, leveraging Eutelsat’s GEO assets for hybrid services.

The customer base is government, maritime, aviation, mining, and telecom backhaul. Pricing reflects the enterprise positioning. OneWeb terminals are larger and more expensive than Starlink consumer dishes; the throughput per terminal is higher.

For markets where Starlink isn’t licensed or where enterprises want a non-Musk-owned operator for political or contracting reasons, OneWeb is the realistic alternative.

IRIS²: European sovereign constellation#

IRIS² (Infrastructure for Resilience, Interconnectivity and Security by Satellite) is the European Union’s response to American (Starlink, Kuiper) and Chinese constellation dominance. The 2023 award designated a consortium led by Airbus, Thales Alenia Space, OHB, Eutelsat, SES, Hispasat, and Telespazio to build a multi-orbit constellation for European sovereign use.

The IRIS² timeline targets initial service around 2027-2028, full operation by 2030, with 290+ satellites across MEO and LEO. The mission scope covers government secure communications, commercial broadband to underserved European areas, and ancillary services.

The 2026 status: design and development with first satellites entering production. The political and financial framework is set; execution risk is real but the EU’s commitment is firm.

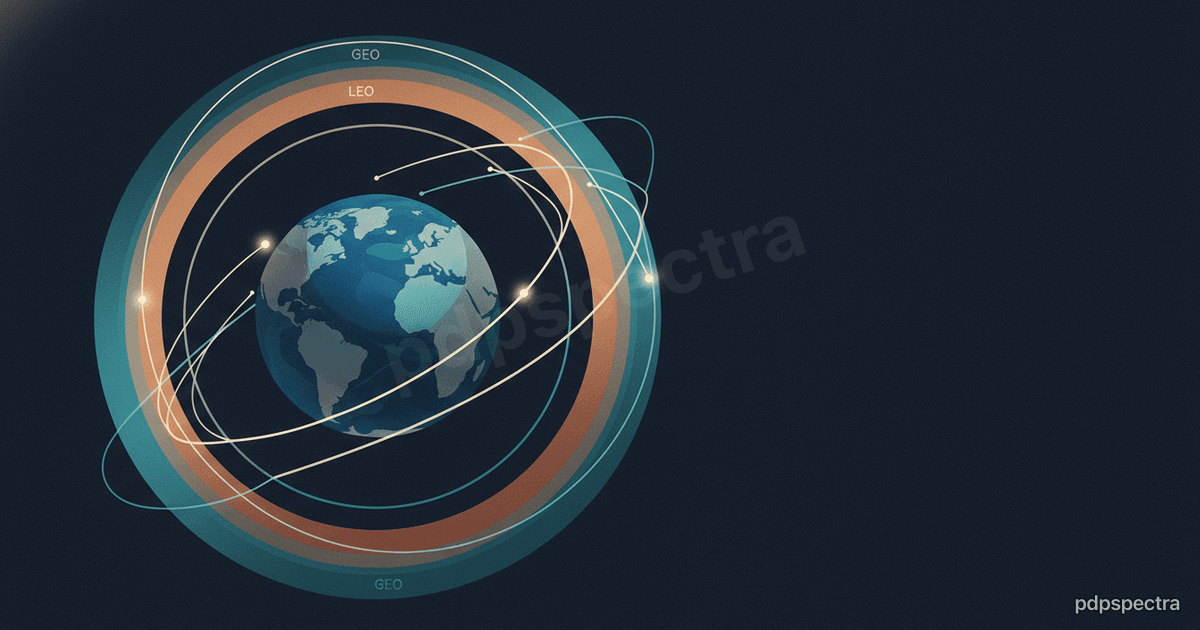

SES O3b mPower and the MEO play#

SES, after its 2024 merger with Intelsat, operates O3b mPower at medium Earth orbit (8,000 km altitude). MEO is a middle ground between LEO (high capacity, more satellites needed, ~550 km) and GEO (high coverage per satellite, high latency, ~36,000 km).

O3b mPower targets enterprise mobility, cruise, government, and high-throughput specialised use cases. The latency is lower than GEO (~150ms vs ~600ms round trip) and the per-satellite capacity is higher than LEO. The constellation is small (a couple dozen satellites) but each is a serious bus.

The 2026 read on MEO: niche but durable. Not going to displace LEO for consumer broadband, but for specific enterprise mobility and government contracts, MEO has real advantages.

GEO incumbents pivoting#

The traditional GEO operators (Hughes Network Systems, Viasat, SES, Intelsat, Hispasat, ABS, AsiaSat) have had to pivot. The consumer broadband business that funded their satellites is structurally smaller. The new strategy:

- Mobility — aviation, maritime, rail — where GEO terminals are already installed and switching costs are high

- Government and military — long-term contracts, broadcast quality, established relationships

- Broadcast — direct-to-home TV is shrinking but still material in some markets

- Multi-orbit play — combining GEO with LEO and MEO assets for differentiated service

Viasat after the Inmarsat acquisition is the most explicit multi-orbit GEO operator. Hughes-EchoStar’s broadband business has shrunk meaningfully while EchoStar’s terrestrial spectrum becomes the more interesting asset.

AST SpaceMobile and cellular-from-space#

AST SpaceMobile is the public-company competitor to Starlink Direct-to-Cell in the cellular-from-space category. AST has signed agreements with AT&T, Verizon, Vodafone, Rakuten, Bell Canada, Telefonica, MTN, Telstra, and many others — covering more than 50 mobile operators globally.

AST’s satellite design is fundamentally different: very large phased-array antennas (~64m² per satellite) compared to Starlink’s smaller Direct-to-Cell payload. The bet is bigger antenna = more capacity per satellite, even if fewer satellites are in orbit.

By early 2026 AST has the BlueWalker 3 demonstrator on orbit and BlueBird-1 satellites operational, with the broader fleet rolling out. The race against Starlink Direct-to-Cell is the most-watched competitive battle in space telecom.

LEO vs GEO economics in 2026#

For decision-makers comparing constellations, the broad economic comparison:

| Dimension | LEO (Starlink, Kuiper, OneWeb) | MEO (O3b mPower) | GEO (Viasat, SES, Hughes) |

|---|---|---|---|

| Latency | ~20-40 ms | ~150 ms | ~600 ms |

| Per-terminal capacity | Mbps to ~1 Gbps | Hundreds of Mbps | Tens of Mbps typically |

| Coverage per satellite | Small | Medium | Hemispheric |

| Satellites needed | Thousands | Dozens | Single-digits per orbit slot |

| Terminal cost | Lower | Higher | Variable |

| Capex per Gbps delivered | Falling fast | Stable | Higher |

The LEO economics keep improving as launch costs fall and constellations scale. GEO economics are improving more slowly. The competitive ceiling for GEO is the markets where the economics differential doesn’t outweigh switching costs.

Sovereign constellation politics#

A 2026 trend that matters: governments increasingly view satellite connectivity as strategic infrastructure, not a commercial good. The EU’s IRIS², China’s national constellations, India’s space programme expansion, Brazil’s interest in sovereign constellation, the UAE space programme — these all reflect the same view.

The economic implication: a global market that looked like it might consolidate to two or three operators (Starlink, Kuiper, OneWeb) is fragmenting along sovereign lines. Each major political bloc wants its own constellation or guaranteed access on terms it controls.

What we tell clients#

For enterprises and governments sizing satellite connectivity in 2026:

- Treat Starlink as the realistic default for most commercial use cases

- Plan for multi-orbit by 2027-2028 when Kuiper is operationally credible

- Consider OneWeb or O3b for non-US operator preference or specific enterprise mobility cases

- Watch IRIS² if you operate in European regulated sectors

Our cloud infrastructure work covers the edge architecture that integrates LEO terminals with the broader network stack.

Related reading#

- Starlink economics in 2026: subscribers, margins, V3, Direct-to-Cell

- Earth observation business in 2026: Planet, Maxar, BlackSky, Capella

- 5G private networks for industrial sites

Satellite constellations in 2026 are no longer a single-operator market. If you’re integrating LEO and multi-orbit connectivity into a distributed operation, our cloud and infrastructure team designs the architecture that makes it work. Tell us about the deployment.